Indigenous enterprises can be categorised into three main categories:-

- Those owned and operated by Indigenous individuals or “nuclear” families where profits may be distributed to individuals;

- Those owned and operated by “communities” or larger Indigenous cultural family groups that are operated for the benefit of the whole group and do not result in distributions of profit to individuals; and

- Those owned and operated by Indigenous corporate and service entities and Prescribed Bodies Corporate where profits may be distributed back to that particular corporation or service entity or its constituent corporate members such as the previously mentioned “communities”.

This article deals with the structuring of the second and third categories. The first category is not dissimilar to the traditional individual business model and structuring for that category will depend on normal commercial considerations such as risk, tax, and business succession as applying to individuals.

The second and third categories are more akin to “public companies” where the structural considerations, apart from cultural considerations, need to consider continuity as well as risk, tax and business succession as applying to a large corporate group.

The common issues tend to be:-

- Multiple types of business may be operated;

- Non-linear growth, where the early years may concentrate on one business and then multiple businesses may suddenly emerge;

- The need to funnel profits back to a central organisation or corporation for it to deal with in accordance with its own Constitution;

- The probability of employing multiple non-Indigenous or at least “not-connected-to-central-organisation” managers for some or all of the different business lines;

- The need for transparent governance through the group, including clear delineation of management responsibilities;

- The need to protect the central organisation and its assets from business failure of an inter-related business;

- The need to build in partnerships and joint ventures with others, whether part of the central group or otherwise;

- The possibility of “hiving off” some of the business elements in future.

In almost all cases we have had experience of, there is a central educational issue surrounding “ownership” and what that entails, as compared to the legal sense of ownership.

Members of the central organisation which owns a business entity that in turn may own one or more businesses are almost always not understanding of the “western” legal issues around the fact that it is the organisation that owns the entity and not themselves per se. In our experience, whatever structures are provided, this educational issue is required at the beginning, and throughout the life of the business, alongside the training in governance so that those “members” can be trained to make their voices heard “appropriately” at the meetings of the central organisation rather than those of subsidiary entities.

As a result of our experience, we believe the central principles surrounding any structuring exercise are:-

- Ensuring the businesses are in appropriate and separate entities themselves, so as to “quarantine” effects of any business failure;

- That these separate businesses are owned directly by the central organisation and not by any “trustees” or “nominee shareholders”;

- That where income tax needs to be paid, to register accordingly;

- That there should be a central “Charter” of how Boards of subsidiary entities need to be comprised and how they need to conduct themselves in relation to the central Board;

- That any managers be required to sign employment contracts that include reporting responsibilities to their Boards, which are all of a similar template through the group.

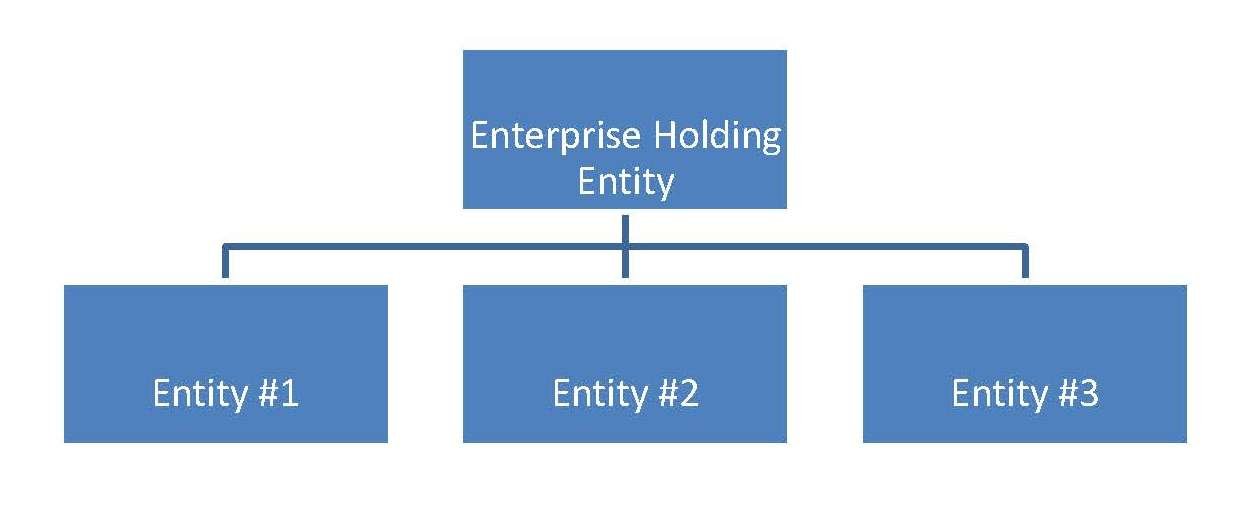

The following is a “template” of a group structure that should be agreed to up front by the central Board so that as any new business activities are considered, the strategy for incorporation and operation is already set.

The Enterprise Holding Entity (“EHE”) should be owned 100% by the Central Organisation (not by members of the Central Organisation as individuals or trustees) so that there is a clearly defined ownership by the larger group and clear profit flows.

The EHE is interposed between the Central Organisation and the entities actually operating businesses so that:-

- There are clearly separate responsibilities of the two different Boards, one of responsibility for all aspects of the central organisation including its enterprises, the other of being solely responsible for enterprise activity;

- There is an interposed “second line of defence” in the case of any business failure and insolvency down the line;

- Accumulated profits can “rest” at this level so that part can be distributed up the line to the central organisation and part can be retained for further enterprise investment, the ratio to be decided as circumstances demand.

As businesses start, they are incorporated into subsidiary entities (herein noted as #1, #2, etc) so that:-

- Each separate business is quarantined from others (and EHE) as well as the central organisation in the event of business failure and liquidation – it is therefore important that cross-guarantees and collateral should not be given;

- Each business entity can have a Board that (perhaps smaller) concentrates only on its responsibility of running that single business and is answerable to the EHE Board for performance;

- Each business can have distinctly separate staff and employment contracts etc as may be necessary if they are in markedly different industries;

- Each entity can be funded separately as required;

- Each entity can be “hived off”, sold, closed, expanded, or partnered/joint ventured with an outside partner/investor without allowing that outside party into the affairs of any other business.

Land assets of the central organisation can sometimes be held in a totally separate non-trading entity. This might be applicable for example in the case of any freehold land that is considered part of the central “estate” that may never be sold. In this case, we believe the best structure is to create a “sister” entity to the Central Organisation but not connected by any ownership, where that land holding entity is owned by all the members in the same way that the Central Organisation is “owned” by the members. There should be no connection to EHE. This sometimes causes issues where the Central Organisation needs to borrow money to fund enterprise as some of this land may be required as security. This needs to be looked at separately should the need arise.

The type of entity that EHE and its subsidiaries should be will depend on a case by case review of circumstances. It should be noted that the EHE and all of its subsidiaries may end up being each totally different legal entities – the point is that each should suit the requirement for its position.

The types of entities possible and their characteristics are:-

| Entity | “Owners” | Surpluses | Control | Tax |

| Aboriginal Corporation | Members (accepted and on register) | Stays in | Board, elected by members | If PBI none; else 30% |

| WA Incorporated | Members or corporations (as accepted and on register) | Depends on Constitution | Committee, elected by members | If PBI none; else 30% |

| Pty Ltd or Limited | Members or corporations (evidenced by shares held) | Dividends to members or “Retained” | Board, elected by members | 30% |

| Limited by Guarantee | Members or corporations (evidenced by being on register) | Dividends to members or “Retained” | Board, elected by members | If PBI none; else 30% |

| NT Bodies | Legislation | Legislation | Legislation | Should be PBI |

| Discretionary Trust | None | To “Beneficiaries” as defined in Trust Deed | Trustee – who appoints? Pty Ltd? | Beneficiaries pay tax on distribution received |

| Fixed Trust | Members or corporations (evidenced by holding “units”) | To Owners of the units | Trustee – who appoints? Pty Ltd? | Beneficiaries; if owned by PBI maybe 30% |

Clearly, a corporate structure consisting of an EHE and multiple subsidiaries under a central organisation could be a recipe for disaster in terms of control and strategic direction. Therefore it is important that before these entities are created, a “Charter” be agreed upon so that as these entities are incorporated, as far as the law allows, the central agreements of the “Charter” are included in the various constituent documents or Constitutions.

We believe the following should be included:-

- The constituency of the EHE Board, nominating stated officers of the central organisation Board to the EHE Board, the need of “independent” members, the number and terms of Board members, etc;

- The constituency of the subsidiary Boards, for example that the subsidiary Boards must include x number of members who are also members of the EHE Board, that there are restrictions to the number of Boards one individual may sit on, etc;

- Rules about Chairmanship for example no single individual can be Chair of more than 2 Boards, and Chair of central organisation may not be Chair of any enterprise Board, etc;

- The requirement for all Board members to attend and keep up to date with Governance and Finance Training within a set time-frame of membership;

- The requirement for the subsidiary Boards to report using templated formats to the EHE Board at set times;

- A minimum ratio of dividends or profit distribution be written into the constitution, subject to waiver by the EHE or central organisation due to the need to establish new businesses or fund capital spending;

- The requirement for Boards to be measured under agreed Performance Measures.

While it is important that each separate business be allowed to run their business in the way they see fit, nevertheless, it is equally important that the strategic direction and indeed the day to day operation of these businesses follow the strategic direction set by the central organisation through the EHE, and that common values are being followed. The “Charter” by which the separate Boards operate will help in this.

Further, without limiting the independence of the different business units, we believe that the contracts of the business unit managers need to follow a common template so that all managers employed in the structure follow common goals and measurements. This employment contract template should also specifically spell out reporting and strategic responsibilities such as:-

- They have to prepare Business Plans with Financial Projections using standard templates at the beginning of each year;

- They are to provide reports following a group template at set times which will report on matters such as actual to budget and explanations of variances, human resources issues, marketing and business opportunities, and so on;

- Performance against agreed Performance Measures.

There could be any number of objectives to be achieved by the central organisation in starting enterprises, ranging from funding its community or charitable activities, increasing economic opportunity for individual members, and so on. It is important to note however that in our opinion, while the EHE and subsidiary businesses should subscribe to the values of the central organisation and operate within its Indigenous culture as well as its corporate culture, they do not have objectives of being a community organisation nor of a charity. In other words they need to be run like businesses (albeit Indigenous businesses that subscribe to Indigenous community culture) that have the objectives of growing the business and investment funds, and making a profit. As the profits are distributed, what the central organisation does with that profit is outside the scope of the EHE structure.